Newsletter commentary Aug 2023

Time:2023-09-06

Time:2023-09-06

An end may bring more endings, but it may also bring new beginnings

In August, during the previous weekend, the China Securities Regulatory Commission (CSRC) introduced regulations to standardize share reduction measures, coordinate the balance between the primary and secondary markets, and the stock exchanges lowered the financing margin requirements. Prior to the implementation of these policies and before the Ministry of Finance reduced half of the stamp duty, the market experienced a continuous decline, with extreme pessimism prevailing. The northbound capital set a record for consecutive selloffs, and the theory of market collapse resurfaced. The poor economic data in July further popularized these viewpoints.

This year's situation has proved to be more complex than anticipated, with the destructive and influential factors stacking up and surpassing our expectations. However, we do not agree with the extreme pessimistic notions implied in stock prices. Over the past period, the lingering effects of the pandemic, prolonged downturn in the real estate industry, sagging employment data, geopolitical uncertainties, and operational difficulties faced by businesses have contributed to a decline in revenue expectations in certain sectors. These objective factors have prompted adjustments in consumption and investment behaviours among economic entities. Coupled with the amplification in public discourse, there has been mutual reinforcement, exerting significant pressure on RMB assets.

These factors have some objective realities supporting them, but they do not represent the real picture. For example, even with poor export data in July, when considering price factors, the actual situation is much better than what the data portrays. The pressure on the RMB is influenced by the significant interest rate differential between China and the United States. The economic cycles of the two countries are not synchronized. Over the past four years, the United States has had a fiscal deficit of nearly 40%, with nearly 8.6% in the past year alone, while its economic growth rate has remained around 2%. High inflation has boosted nominal GDP and the income of economic entities. China has relatively low-price levels, which makes it challenging for income growth among economic entities. However, considering production capacity itself, it is difficult to say that the Chinese economy is doing poorly. One situation may appear favourable while the other seems unfavourable, indicating that it is not as simple as it appears.

Real estate has been the most important savings medium for a long time. Governments, businesses, and households have used real estate as a concentrated savings, converting them into houses, infrastructure, and factories through investment. This has been a common model that most local governments have been able to implement. However, as the real estate market reaches its peak, this model is diminishing. The transformation of savings into investment now requires the vision and insight of governments. For example, the government of Hefei city of Anhui Province. This is not a universally applicable model, and in the future, not everyone will need to emulate the Hefei government's approach. As China's economy moves further away from a phase of comprehensive investment, more emphasis will be placed on the transformation from savings to consumption. This transition process requires adaptation from all economic entities and will take time.

The role of governments at various levels in the Chinese economy is often underestimated. Policies play an essential and undeniable role in our economic operations. However, the formulation and implementation of government policies require observation and adaptation periods, especially during significant transformations, for instance the changing landscape of the real estate sector. Both the government and residents and businesses need time to understand and digest the current changes.

Recently, we have witnessed the gradual implementation of many policies that the market has been anticipating. These policies have exceeded expectations in terms of their scale and impact. Based on past experiences, policies are often endogenous and may sometimes be delayed. It is normal for this to happen in the current complex situation.

In addition, the real estate sector around 2015-2016, Vanke, a prominent real estate company, referred to it as the "silver era." During that time, many other real estate companies were also experiencing rapid growth. However, many companies that aggressively leveraged themselves are now facing significant challenges. Nevertheless, just recently, Yu Liang, the CEO of Vanke, has stated that the real estate market has already overshot its decline. He mentioned that the new construction area of residential properties nationwide has declined by 11% and 40% in 2021 and 2022, respectively. From January to July this year, it further decreased by 25%. Based on this downward trend, it is projected that the new construction area for this year will only be around 660 million square meters, returning to the level of 2006, which was back to seventeen years ago.

It is likely that the new construction phase in the real estate sector has reached a low point, but the transmission of the existing inventory throughout the entire real estate chain will continue for some time. Since the development stage of the real estate market has changed significantly, the necessity of restrictive measures has also evolved. While the total stock of real estate is indeed substantial, there will be a long-term demand for improved housing driven by the aspiration for a better quality of life. Policies such as down payment requirements and mortgage regulations still have room for optimization (as mentioned in the recent news, relevant authorities have announced adjustments to these policies). Overall, in our view for the real estate sector is not overly optimistic, but the most challenging phase of real estate's drag on the economy will eventually pass.

Moving into the issue of local government debt, the current difficulties faced by the central government are not as significant as those before the introduction of the tax-sharing reform in the 1990s. In terms of our current overall financial capacity and high savings rate, the problem is not a matter of quantity. The real challenge lies in rebuilding the incentive constraints during the process of central government assistance and how to prevent moral hazards and adverse selection by local governments. This issue is similar in nature to a parent calling a family meeting to distribute fruits among family members. It is something that will inevitably happen, and parents expect family members to be self-reliant and mutually supportive in times of hardship, but there is no mechanism that can work effectively in the long run. However, after solving a particular problem, the creation of a new constraint mechanism that works for a certain period is desirable, as like the tax-sharing reform in the 1990s. We look forward to the optimization of rights and responsibilities between the central and local governments, adapting to new requirements for high-quality development and domestic circulation.

Turning to the issues in the financial system, based on limited observations, the level of thoroughness in decision-making within the financial system is much higher than that of market discussions. For example, the discussion on bank interest spreads in monetary policy reports and the response from the China Securities Regulatory Commission to the call for T+0 trading. Bank interest spreads have limited room for further decline, and one-sided concessions are no longer sustainable. Banks' return on equity (ROE) is around 10-11%, with 30% of dividends being retained as core capital after the loss of equity financing function, barely sufficient for expanding balance sheets to support economic development for the next year. As for T+0 trading, in a market with majority of retail investors in China, further liberalization would lead to excessive short-sighted effect and unnecessary. In the past two years, despite the sluggishness of the A-share market, the turnover rate, when converted to the actual tradable portion, still stands at around 7-8 times, compared to around 2.5 times in the US market. From this perspective, our market is already quite active.

The recent regulations by the China Securities Regulatory Commission (CSRC) regarding share reduction represent a significant institutional change. It signifies a major rebalancing of the investment and financing functions of the stock market. The incentive mechanism for major shareholders has shifted to "if you can bring prosperity to small and minority shareholders, then you can benefit from the stock market to create wealth. If you cannot achieve this, then you cannot rely on the stock market to increase your wealth because it easily turns into redistribution rather than creation." In the new era of market transition, this design promotes a more balanced distribution of rights and responsibilities.

Restrictions on major shareholders are common in many markets. Some markets may even stipulate that major shareholders are not allowed to reduce their holdings before distributing dividends that exceed the amount of financing. As a country that relies on the capital market for industrial upgrading, there is an increasing demand to allow the public to obtain sustainable property income through the capital market. Therefore, it is necessary to rebalance the interests of investors in earning profits and the need to pool savings for innovative investments. The timing of the introduction of these policies is opportune, given the current circumstances.

In the past, the conversion of savings into investment did not require much attention to whose savings it was. It was more of a concept related to the overall quantity. However, when savings are converted into consumption, the ownership of savings becomes important. Both the total amount and the structure of savings become substantial. In the past, real estate was the primary investment vehicle of wealth for everyone. In the future, the proportion of financial assets is expected to increase. Therefore, the health of the capital market is closely linked to the successful transformation of industrial upgrading and the development of the domestic circulation. We believe that these factors are also endogenous to the system.

Meanwhile, there is a subject of debate whether the capital market can represent a vital generator. Some people lightly mock at times-even the market for hovering around the 3000-point level for numerous years. However, this perception does not reflect the actual reality. The limitations of index construction have led to misunderstandings among many people. As a predominantly manufacturing-based economy, it is true that there are not many companies experiencing sustained bull markets. However, there are still quite a few companies that have started small and grown significantly over time. Some indices may frequently engage in buying high and selling low, underestimating the long-term value creation.

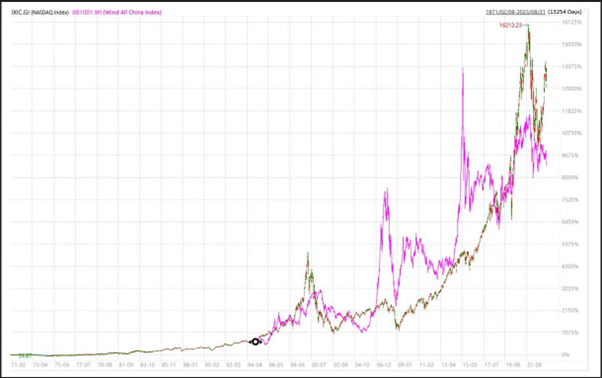

The chart above shows that the Wind All China Index, when compared to the highly renowned Nasdaq market, holds its own and performs well. Particularly, it has been on par with the Nasdaq market, especially before the AI market boom this year. The Wind All China Index is a free-float market-cap-weighted total return index. The notable difference lies in the volatility of the Wind All China Index. If the long-term trend implies value creation and innovation capabilities, then we can indeed be considered outstanding.

If we simply divide the A-share market into two main categories, one consists of state-owned enterprises (SOEs) and similar companies, accounting for about half of the profits. This category has seen growing performance for a long time, but valuations have been declining. Particularly banking stocks are a typical example. It has not been easy for investors to make money, and considering dividends has been a slightly better option. However, the recent evolution of assessment methods by the State-owned Assets Supervision and Administration Commission (SASAC), the new rules on reducing holdings issued by the China Securities Regulatory Commission (CSRC), and other incentive measures are meaningful for activating the investment value of this part of stocks. In the future, with low expectations for interest rates, many companies have passed their investment peaks, and the investment value will be further highlighted.

The second category consists of companies with great creativity but high stock price volatility. It is common for these companies to go several years without reaching new highs, resulting in a poor investment experience. Reducing volatility can increase investment value in the same economic conditions. This process involves discussions on introducing long-term funds and assessment methods.

Moreover, if there is a mechanism to reduce volatility, in terms of increasing the power of balancing long positions, making significant changes in analyst incentives and the ease of short selling, and potentially lifting the 10% daily limit on price fluctuations, which may initially appear to amplify volatility but could ultimately lead to reduced volatility (this requires further rigorous analysis to be approved). If the volatility of these companies decreases, their investment attractiveness can be significantly enhanced. To sum up, the increased investment opportunities in both categories of stocks can enhance the overall investment landscape. In the same economic environment, the investment value of stocks can undergo substantial changes.

Apart from familiar factors such as education, technology, industry, and defence capabilities, financial capability is also a crucial aspect of competition between nations. In the past, real estate helped facilitate the transformation from savings to investment. In the future, the role of the capital market will naturally increase. This is because it involves determining which companies receive funding, enabling the desired industrial upgrading. Simultaneously, it allows investors to have stable property income and completes the cycle of savings, investment, and consumption. A well-functioning capital market is a necessity in achieving these objectives.

China's economy has been sprinting ahead for several decades, covering a distance that took other countries hundreds of years to traverse. Other nations have faced challenges like the Great Depression, world wars, and financial crises. In comparison, China has achieved a relatively stable economic environment. The current challenges we are experiencing are part of the necessary path of major macroeconomic adjustments, and such transitions are never easy.

At the same time, a portion of savings will be used for consumption. The ability to consume depends not only on the total amount of savings but also on the distribution of savings among individuals. Increasing the consumption rate requires ensuring that more people share in the benefits of social and economic development, thereby increasing their consumption capacity and promoting high-quality development and domestic circulation. Activating existing assets will enhance financial resources, further improving public service capabilities. The capital market also serves as a crucial intermediary in this process.

A more efficient capital market that effectively balances investment and financing functions will become a fundamental component of our high-quality development. In this scenario, small and medium-sized shareholders will naturally benefit from these developments.

In the past, high savings were indirectly converted into investment and net exports through real estate and indirect financing. In the future, savings will need to be transformed into investment through direct financing using financial products. This requires increasing precision and entails greater project risks. Ultimately an efficient capital market serves as a crucial intermediary for this transformation.

Simultaneously, a portion of savings will be used for consumption. The ability to consume depends on individual financial capacity, whereas the conversion into investment and net exports does not depend on the source of the funds. Increasing the consumption rate not only relies on the total amount of past savings but also on the distribution of savings.

By allowing more people to share in the benefits of social and economic development, increasing consumption capacity contributes to high-quality development and internal circulation. Activating existing assets enhances financial resources, further improving public service capabilities. The capital market also serves as a crucial intermediary in this process. A more efficient capital market that effectively balances investment and financing functions will become a fundamental component of our high-quality development. As a result, small and medium-sized shareholders will naturally benefit from this configuration.

When the door to the real estate market closes, another door to the capital market will open. However, the market's performance seems to suggest that the door no longer exists. We have more faith in the opening of the other door, even though it may not happen immediately. We maintain strategic expectations and exercise tactical patience.